Banks are no longer just financial institutions that takes deposits, offers loans and provides essential financial services. They are technologically advanced institutions as well, handling huge amount of data, transactions, mobile apps, APIs, and third-party integrations.

As we move toward 2026, this dependence on technology is reshaping Banking Cybersecurity in ways that are both exciting and risky. Attackers are very smart, quick and more organized than before, while banks now face the ultimate challenge of staying ironclad against threats without slowing down the digital experience.

This blog breaks down the key cyber threats that banks are likely to face by 2026 and the defence strategies that can actually help.

Why Banking Cybersecurity Matters More Than Ever?

From people wanting instant payments to wanting seamless apps, the rise of Digital Banking has changed the expectations of the customers.

For cybercriminals, banks remain high-value targets. A single breach can lead to financial loss, reputational damage, regulatory penalties, and long-term trust issues.

That is why Financial Cybersecurity is no longer just an IT responsibility. It has become a core business priority as well

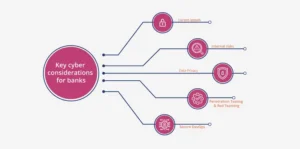

Emerging Cyber Threats Faced by Banks

1) Advanced Phishing and Social Engineering Attacks

Phishing is evolving fast. By 2026, it is expected that attackers will be using AI to craft highly convincing and super realistic emails, messages, and even voice calls that fool both customers and employees, often bypassing basic security awareness training.

Bank staff with access to internal systems are especially targets. One click can really be risky.

2) Ransomware Targeting Core Banking Systems

Ransomware has moved beyond encrypting files. Modern attacks aim to destroy operations, steal data, and pressure banks into paying by threatening public leaks.

In 2026, ransomware groups are likely to focus on critical systems such as payment gateways and customer databases. This directly impacts Banking Security and business continuity.

3) API (Application programming interface) and Open Banking Vulnerabilities

Open banking has improved customer choice and innovation, but it has also increased the attack surface. Poorly secured APIs can sensitive data or allow unauthorized transactions.

As more banks rely on fintech partnerships, managing third-party risk will be a major Cyber Defense challenge.

4) Insider Threats and Privilege Misuse

Not all threats come from outside. Employees, contractors, and vendors with excessive access rights can unintentionally or intentionally cause security incidents.

With remote and hybrid work becoming standard, monitoring user behaviour without invading privacy is becoming harder for banks.

5) Cloud and Configuration Risks

Banks are moving workloads to the cloud for scalability and cost efficiency. However, misconfigured cloud storage, weak identity controls, and poor visibility remain common issues.

Many breaches are not caused by advanced hacking but by simple configuration mistakes that expose sensitive data.

Regulatory Pressure and the Role of RBI

India’s RBI is ramping up the heat on cyber resilience. Their guidelines now demand routine security audits, swift incident reporting, tight vendor oversight, and boardroom accountability.

By 2026, expect even tougher rules on data protection, resilience drills, and rapid response prep. It’s a global push too as international banks are scrambling to keep up.

Cyber Defense Strategies for Banks

1) Zero Trust Security as a Foundation

Zero Trust is no longer a buzzword; it has become a necessity. This approach assumes that no user or system should be trusted by default.

Banks are adopting identity-based access, continuous verification, and strict privilege controls to reduce lateral movement during attacks.

2) Stronger Identity and Access Management

Identity is the new perimeter. Multi-factor authentication, privileged access management, and regular access reviews are critical.

By 2026, banks that fail to modernize identity controls will struggle to contain breaches once attackers get in.

3) Real-Time Monitoring and Threat Intelligence

Traditional security tools are not enough as banks need real-time visibility into network traffic, user behaviour, and system activity.

Threat intelligence feeds, combined with behavioural analytics, help security teams in detecting patterns early before damage happens.

4) Secure-by-Design Digital Banking Platforms

Security can no longer be added after development. Secure coding practices, regular penetration testing, and automated security checks must be part of the development lifecycle.

This is important for mobile apps and online platforms that form the core of Digital Banking services.

5) Employee Awareness That Goes Beyond Training

Sessions on annual awareness are not enough as banks need continuous, role-based security education that reflects real attack scenarios.

Employees who understand the pattern of how attackers operate, they become an active part of the defence strategy.

6) Data Protection as a Competitive Advantage

Customers have become more concerned and aware than ever before. Banks investing in encryption, data loss prevention, and strict data governance tends to build trust over time.

Looking Ahead to Banking Cyber Security- 2026

The future of Banking Cybersecurity will be created by automation, regulation, and collaboration. Banks will work with regulators, fintech partners, and cybersecurity providers to stay ahead of threats.

One cannot deny the fact that strong Banking Security will not just protect systems but it will also protect customer confidence, brand reputation, and the stability of the financial ecosystem itself.

Comments

Join the discussion. We’d love to hear your thoughts.